CONCEPCIÓN, Chile — The churning blast furnaces of shrinking steelworks and the glowing flare stack of an oil refinery mark the aging industrial landscape around Concepción in southern Chile. Not long ago, a historic ceramics factory shut its doors here.

But the seeds of a potential revival lie just below the wooded hills overlooking this Pacific-facing city. This is where a mining venture called Penco, led by Toronto-listed Aclara Resources, is proposing to extract rare earths, the unique elements needed to make the magnets in everything from electric car motors and wind turbines to Lockheed Martin-manufactured F-35 fighter jets and MRI machines.

The $130 million Penco project offers a potential “quick win for the West” that needs sustainably mined critical minerals from friendly jurisdictions, Aclara CEO Ramón Barúa Costa told AQ. The company and its Chilean partner, steelmaker CAP, have just reapplied for an environmental permit that they hope Chilean authorities will swiftly approve after an initial submission ran aground to get the first project module up and running by 2028.

Penco is part of a regional trend gathering steam—not only in Chile but more prominently in Brazil—to break the near-total control China maintains over rare earths. As the U.S. seeks to decouple manufacturing from the Asian giant and global industry shifts to producing new and greener products like electric vehicles, establishing reliable Western supply chains for rare earths supply looks to become a strategic imperative.

Miners say the ionic clays and monazite rocks in parts of Chile and Brazil hold the ideal mix of rare earths to make magnets. And while China has been criticized for environmental practices in mining rare earths at home and in Myanmar, the emerging crop of Latin American ventures promises to tap rare earths sustainably. Automakers from General Motors Company to Toyota and budding magnet manufacturers have been trotting through Chile and Brazil, exploring potential supply alternatives outside China. Especially appealing are South America’s heavy rare earths, dysprosium and terbium, which are less abundant than light rare earths found in the U.S. and Australia.

The automakers “used to shake our hands and say goodbye. Now they want to hear more,” one South American mining executive, who preferred to remain anonymous due to sensitive business concerns, told AQ.

Rising appetite

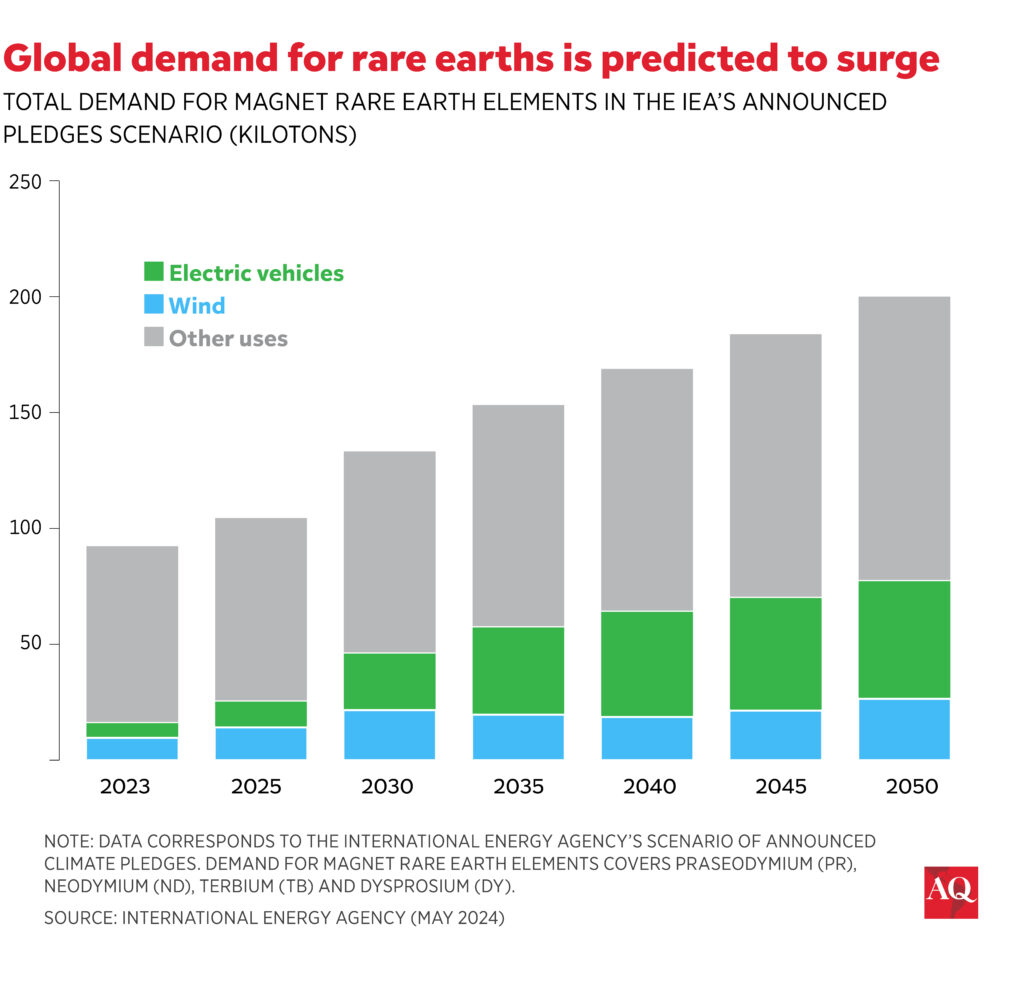

The data shows why. Between 2015 and 2023, the global appetite for magnet rare earths nearly doubled to 93,000 tons and is predicted to surge by more than 80% to 169,000 tons in 2040, driven mainly by EV motors, according to the International Energy Agency’s scenario of announced climate pledges.

The IEA says the world faces less risk of a supply deficit for rare earths than for battery metals copper and lithium, which also abound in Latin America. However, rare earths are subject to “an extremely important level of geographical concentration” of current and future mining and refining projects “that expose this market significantly to supply disruptions.”

However, these fundamentals are not reflected in the current prices of rare earths. Experts say that to maintain its grip over 70% of the world’s production and 90% of processing, Beijing keeps prices artificially low, which is too low for alternative suppliers to turn a profit.

“At these current price levels,” said Brian Menell, CEO of Dublin-based technology metals investment company TechMet, “most Western producers, and likely some Chinese producers, are operating at a loss.”

Rare earths in Brazil

Although Brazil’s government has been supportive, operations there are off to a bumpy start. In Goiás, ramp up for first-mover Serra Verde Group, a venture controlled by U.S. private equity, has fallen short of expectations. The company’s travails impact its Chinese offtaker, but they could hurt competitors more by undermining investor confidence.

Serra Verde is coy about its operational status. “Despite Serra Verde’s success in getting past the starting line first, it is still a nascent sector which will require continued support to establish itself in a highly competitive market,” CEO Thras Moraitis told AQ in an email.

Undaunted, Toronto-based Neo Performance Materials plans to purchase 3,000 metric tons per year of rare earth oxide from Australia’s West Perth-based firm Meteoric Resources’ Caldeira project in Minas Gerais state. The rare earths will supply a magnet plant that Neo is developing in Estonia.

In neighboring Bahia state, Colorado’s Lakewood-based uranium producer Energy Fuels plans to excavate rare earths in 2026. The Brazil mine, and projects in Australia and Madagascar, will supply the company’s White Mesa mill in Utah, where it can monetize the radioactive materials accompanying rare earths. “While uranium is a problem for everyone else, it’s actually a value-add for us,” senior vice president Curtis Moore told AQ. “We can recover it and sell it into the nuclear industry.”

Elsewhere in Brazil, Aclara plans to replicate its Chilean project in Goiás state. Other aspirants are Appia, Viridis, and Brazilian Rare Earths.

The U.S. side of the equation

U.S. magnet-making hasn’t thrived, mainly because China guards its technological know-how, and raw material prices have slumped. Since October, Chinese dysprosium oxide prices have tumbled by 25% to just over $300/kg, according to London-based pricing agency Fastmarkets.

But with an eye on supply security, Western governments are stepping in. The Biden administration is imposing more tariffs on Chinese high-tech goods, including a 25% magnet duty in 2026. The Pentagon has granted $430 million to magnet manufacturers like MP Materials, Lynas, and VAC. It’s also exploring AI-based critical commodity pricing as it seeks to establish a domestic mine-to-magnet supply chain to meet all its defense needs by 2027. U.S. overseas investment arm, DFC, has opened shop in São Paulo, defining its mission to “grow its portfolio of investments in key mineral resources,” as it’s already done with nickel.

For Latin America, rare earths offer a chance to diversify and revitalize economies along greener lines. The region could also satisfy its ambitious industrial aspirations by separating and processing rare earths into metals and alloys. It’s now up to Western manufacturers, governments, and investors to consider the underlying value proposition behind the strategic resource.

ABOUT THE AUTHOR

Patricia Garip

Reading Time: 4 minutesGarip is a journalist based in Santiago, Chile. She recently joined Bloomberg News as a regional editor.